The 10 billion dollar freighttech that was promised

Building a universal clearinghouse for freight.

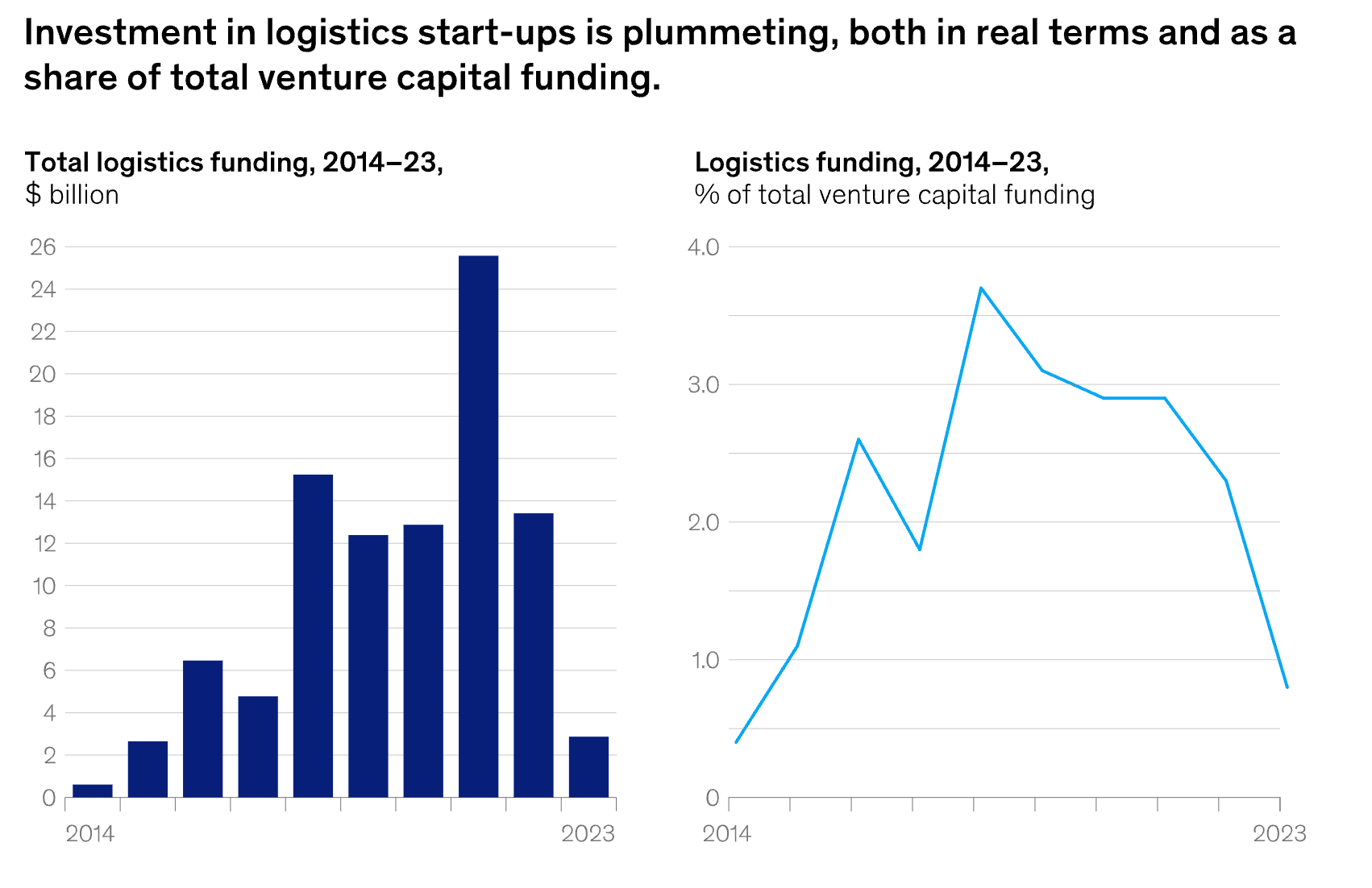

The rearview mirror

The first decade of venture funded “freight tech” could be characterized in many ways, but few would say it’s been uneventful. $100B have been poured into digital freight brokerages, virtual carriers, next generation fuel cards, and tech-enabled freight forwarders. The terminal value of these investments has yet to be proven; though the bankruptcies, restructurings, and business model pivots paint a particularly grim outlook. “Pure software” plays for an individual LSP category (carrier, broker, or freight-forwarder) are simply sub-scale for venture investment, while approaches entirely dependent on spot market GMV are sensitive to freight’s violent demand cycles.

Despite the wreckage in the rearview mirror, it’s hard not to be excited about the road ahead. Over-the-road freight is still a $400B industry, with an estimated $40B of non-driver operational expense spend. Core operational workflows such as quoting, billing, and tendering still occur largely over email or phone. The unbundling of the transportation management system (TMS) presents ripe opportunity for complex workflow automations, living atop the previously impenetrable source of truth. Generative AI enables the digitization of natural language workflows, only recently tractable for incumbent software vendors.

The road ahead

How will the next decade be any different than the last? What opportunities expand beyond meager LSP IT spend without reliance on a marketplace take rate?

AI eats OPEX

One answer has been to build software that competes directly against labor costs. It’s become vogue to build product surfaces mimicking communication with real employees to avoid the typically long implementation and training cycles for vertical SaaS. For many LSP workflows (appointment scheduling, quoting, billing, etc.) overseas outsourcing is already commonplace. These tasks are ripe to be replaced with customized, deterministic, LLM-native applications. They largely involve repeatable execution on a pre-defined set of steps, analyzing unstructured documents and human communication.

While productivity tooling for LSPs is an enticing product opportunity, it remains unclear whether it’s venture scale. A typical brokerage might achieve net revenues of 15%, of which 70% is spent on personnel (~%10 of total). Of this massive headcount budget, 80%, is spent on “high value” tasks: attaining and building relationships with carriers, warehouse owners, and shippers. 20% (~2% of total) is spent on tedious “back office” tasks like appointment scheduling, quoting, load building, document collection, and billing. In aggregate, this is $3.2B of total addressable spend, from the $160B US 3PL industry. Carrier businesses operate similarly, a 10-truck carrier can spend 170K$ outsourcing administrative tasks such as dispatching, tendering, and accounting.

Monetizing freight volumes

While many freight software categories remain highly fragmented with low NPS, the US LSP market is simply subscale for venture outcomes. Attractive freight-tech opportunities directly monetize of shipper freight procurement ($1.3 trillion of US spend) rather than subscription revenue from an individual category. Winning opportunities will facilitate a core data flow for a plurality of freight volume and will monetize with transaction processing or supply chain financing. The sheer variety of counterparties participating in a freight transaction (shippers, forwarders, brokers, and LSPs) allows entrepreneurs to monetize multiple “turns of the dollar”. Each “leg” of the payments journey from shipper to carrier can compound the percentage take of a payments network business.

The “10 billion dollar freight tech that was promised” likely combines these two approaches to construct an entirely novel business model. It will digitize complex and unstructured activity between LSPs and their customers, converting manual back-and-forths into standardized remote procedure calls.

The opportunity in payments

The biggest opportunity to build than integration layer likely exists in billing and payments. This is a business-critical workflow for any high volume LSP and is rarely a “core-competency”. While “pre-delivery” workflows completed by “front-office” staff have been a primary focus for most LSP software offerings (quoting, load building, track and trace), “post-delivery” actions taken after a load “is transferred to accounting” are distant landmarks on most freight tech roadmaps.

It’s often joked that the most common refrain in logistics is “where’s my stuff”, in reference to the critical freight challenge of shipment visibility. The second most common is “where’s my money”. Invoicing for freight services is an operational nightmare, for a number of reasons:

Extreme customer fragmentation requires LSPs to support various invoicing flows, leveraging shipper portals, billing through EDI, over email, even by fax or post.

To generate an invoice, carriers and brokers must retrieve proof of delivery (PODs) from drivers upon delivery at a facility, which satisfy stringent shipper requirements (so far, I’ve seen dozens: documents are required to be scanned, consignee signatures must be circled, all PO identifiers must be legible, etc.). Brokers often bill large shippers in batches of 50-100 shipments, so a single error invalidating a bulk invoice can debilitate 3PL cashflows.

Invoices can include nearly hundreds of miscellaneous charges: carriers can face deductions by failing to track their trip, brokers payout detention **for every hour past an appointment that a carrier waits at a facility, food distributors charge “claims” for fruit spoiled by trailers from minor deficiencies in trailer refrigeration. These “accessorial” charges require detailed unstructured evidence (in-and-out times, receiver notes) to audit and dispute.

Freight payment is often as disordered as billing. Brokers, forwarders, and shippers pay vendors via check, credit card, wire, or ACH. Payers send remittances in a variety of formats and will even mail invoices back to their vendors as a payment notification. Large shippers and brokers will often make payments in bulk, requiring LSPs to stitch together extensive balance reports to accurately reconcile incoming payments.

Most load volume between carriers and brokers is paid by invoice factoring companies. In order for these companies to release a single payment, an operator at a factoring company needs to converse with an operator at a brokerage to verify that the carrier will be paid the invoiced rate, that all documents submitted by a carrier are entirely valid, and that released payment will go to the correct party.

Every manual verification and translation step between members the 4 counterparties of freight procurement (carriers, 3PLs, factors, and shippers) present a transactional monetization opportunity. Transportations factors will pay outsourced agents $1-3 for each invoice they successfully verify, LSP outsourced collections departments can cost 2-4% of net revenue, and shippers can collect high-margin “quickpay” revenue from LSPs, accelerating vendor payment for a percentage of total transportation volume.

A particularly exciting wedge into payments communication is the arduous process of invoice verification for LSP factors. Nearly $90B of freight spend (70% of 3PL volume) is processed by transportation factors that charge 2-3%, smoothing carrier cashflows. Millions of dollars of operating expense is spent between factors and brokers to confirm the amounts of individual invoices. Automating this communication end-to-end had previously been impossible due to extreme counterparty fragmentation. Everyday hundreds of transportation factors work with thousands of brokers using dozens of bespoke TMSes. Recent advancements in LLMs allows a software player to rapidly digitize manual communication over email, phone, and web portal bootstrapping a payments network for instant verification of every load.

The “clearinghouse” for freight

The opportunity to digitize logistics payments communication parallels the rise of healthcare clearinghouses, which charge a per transaction fee for communication between tens of thousands of providers and tens of thousands of payers. Fragmentation in that industry made invoicing, payment verification, and reconciliation painful for businesses giving rise to massive software opportunities like Waystar, Change Healthcare, and Optum. A similar approach in freight yields a similar opportunity to standardize the transmission of accounting information between industry parties. Just as healthcare clearinghouses established a foothold with claims submission, before extending to prior authorization, denial resolution, and payment posting, a “clearinghouse for freight” has the opportunity to “land” in load verification and “expand” into remittance processing and dispute management.

Clearinghouses and payment processors fundamentally rewrote business processes by allowing the transfer of value to move digitally alongside the transfer of money. Insurmountable software fragmentation previously prevented this innovation from reaching supply chain. As the barriers for digitizing unstructured communication begin to fall, opportunity arises for the right team to build a massive defensible network business.

If this opportunity is as exciting to you as it is to me and you’d like to chat more, reach out to Ken Acquah.